Global Semi-Autonomous Autonomous Bus Market Overview

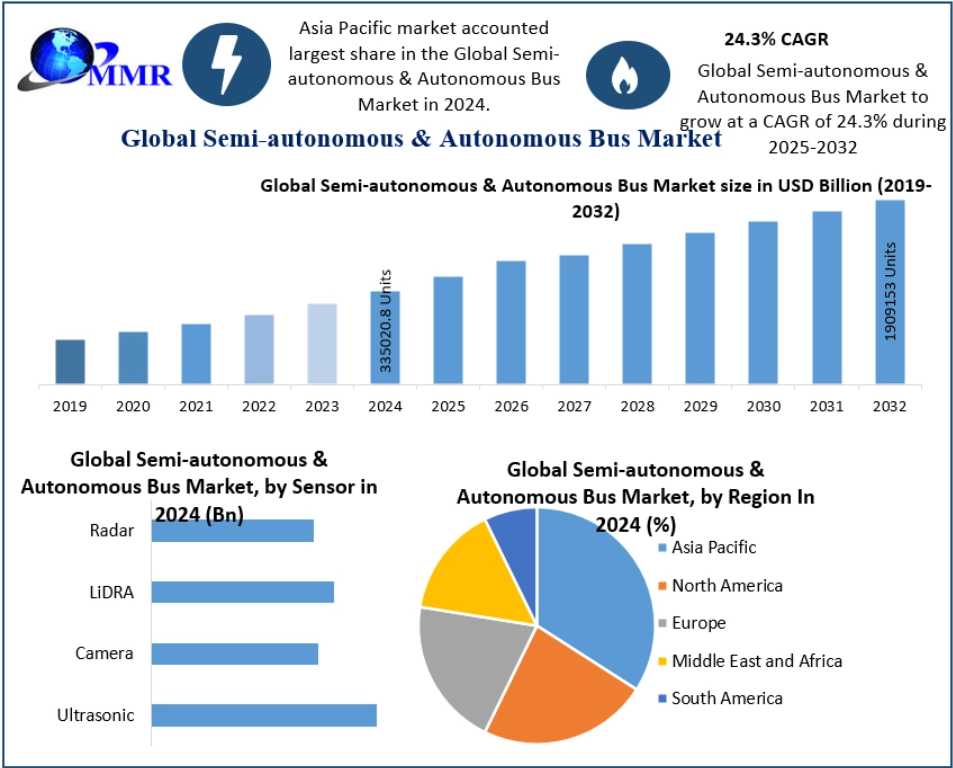

TheGlobalSemi-autonomous Autonomous Bus Marketrecorded a volume of335,020 units in 2024and is projected to expand at a robustCAGR of 24.3% between 2025 and 2032, reaching approximately1,909,153 units by 2032. This exceptional growth trajectory reflects the rapid evolution ofautonomous driving technologies, rising urban mobility challenges, and increasing investments insmart public transportation systems.

Semi-autonomous buses operate with advanced driver assistance features, supporting human drivers under specific conditions, while fully autonomous buses are capable of navigating and operating without human intervention. Together, these technologies are reshaping public transport by enhancingsafety, operational efficiency, passenger comfort, and cost optimization.

Autonomous bus systems are designed to strictly follow traffic regulations, maintain safe distances, and respond intelligently to dynamic road conditions. By minimizing human errorone of the leading causes of road accidentsthese buses are expected to significantly improveroad safety, traffic flow, and overall transport productivity.

Request a Free Sample Copy or View Report Summary:https://www.maximizemarketresearch.com/request-sample/152506/

Market Evolution and Technology Landscape

The autonomous bus ecosystem is witnessing accelerated innovation driven byAI, machine learning, advanced sensors, and vehicle connectivity technologies. Integration of real-time data processing enables buses to adapt to traffic conditions, detect obstacles, and interact seamlessly with surrounding infrastructure.

Urban congestion, rising fuel costs, and labor shortages in the transportation sector are further encouraging transit authorities and operators to exploresemi-autonomous and autonomous solutionsas sustainable long-term alternatives.

Impact of COVID-19 on the Market

The COVID-19 pandemic had a lasting impact on the global public transportation sector. During lockdowns, bus operations were halted across most countries, leading to revenue losses and delayed fleet expansion plans.

Post-pandemic challenges such associal distancing norms, workforce management, sanitation protocols, and reduced passenger confidencehave strained the financial sustainability of bus operators. However, these challenges have also accelerated interest in autonomous buses, which reduce dependence on drivers and enablecontactless, safer, and more controlled transport environments.

As economies gradually reopened, governments and municipalities began re-evaluating public transport strategies, positioning autonomous buses as a key component ofresilient and future-ready mobility systems.

Semi-Autonomous Autonomous Bus Market Dynamics

Key Drivers: Efficiency, Safety, and Cost Optimization

The adoption of semi-autonomous and autonomous buses offers multiple operational advantages:

- Reduced driver fatigue and stress

- Lower labor and operational costs

- Enhanced fleet productivity and utilization

- Improved fuel efficiency and reduced emissions

- Lower accident rates and safer driving behavior

By enabling drivers to transition into supervisory roles or removing the need for drivers entirely, autonomous buses unlock significant cost savings for commercial and municipal transport operators.

Market Restraints: Security, Privacy, and Safety Concerns

Despite strong growth potential, the market faces challenges related tocybersecurity and data privacy. Autonomous buses rely heavily on connected systems, cloud platforms, and real-time data exchange, increasing vulnerability to cyber threats.

Concerns overlocation tracking, data sharing, system hacking, and misuse of autonomous technologyremain key barriers to widespread adoption. Additionally, safety risks involving interactions with non-autonomous road users continue to raise regulatory and public acceptance issues.

Market Opportunities: Rising Adoption of 5G Connectivity

The deployment of5G networkspresents a major growth opportunity for the semi-autonomous and autonomous bus market. High-speed, low-latency communication enables:

- Advanced vehicle-to-vehicle (V2V) and vehicle-to-infrastructure (V2I) communication

- Real-time hazard detection and collision avoidance

- Intelligent traffic signal coordination

- Seamless integration with traffic management systems (TMS)

With 5G, autonomous buses can anticipate road conditions well in advance, improving safety, ride comfort, and traffic efficiency.

Segment Analysis

By Sensor Type

Theultrasonic sensor segmentis expected to hold the largest market share due to itscost-effectiveness and reliability in detecting nearby solid objects. These sensors are widely used for parking assistance, obstacle detection, and low-speed maneuvering, often in combination with cameras.

Thecamera sensor segmentranks second, driven by the growing adoption of360-degree vision systems. Multi-camera setups enable precise detection of vehicles, pedestrians, lane markings, traffic signs, and road boundaries.

Camera technologies include:

- Near-Infrared (NIR) cameras

- Visible (VIS) light cameras

- Thermal cameras

- Time-of-Flight (ToF) cameras

These sensors work best when integrated together, offering redundancy and improved environmental perception.

By Application

Theshuttle segment dominates the market, as autonomous shuttles are already commercialized and deployed in controlled environments such as campuses, airports, business parks, and smart cities.

Leading companies such asNavya, EasyMile, and Local Motorshave successfully launched self-driving shuttle solutions. Autonomous shuttles increase service frequency, reduce operational costs, and enhance passenger safety by maintaining smooth driving patterns with minimal braking and acceleration.

Request a Free Sample Copy or View Report Summary:https://www.maximizemarketresearch.com/request-sample/152506/

Regional Insights

Asia Pacific

TheAsia Pacific regionrepresents one of the fastest-growing markets, supported by technologically advanced automotive ecosystems inChina, Japan, and South Korea. China has emerged as a global leader, with companies likeKing Longachieving volume production of autonomous shuttles in partnership with technology providers such asBaidu.

High reliance on buses as a primary mode of public transport, combined with government support for smart mobility initiatives, positions Asia Pacific as a key growth engine for the market.

Europe

Europe presents strong growth opportunities, particularly forsemi-autonomous buses, driven by upcoming safety regulations mandating features such asAutonomous Emergency Braking (AEB)andBlind Spot Detection (BSD).

The region is home to leading Tier-1 suppliers includingBosch, Continental, and ZF, along with autonomous shuttle pioneers such asEasyMile, Navya, and 2getthere. Extensive pilot programs and favorable regulatory frameworks continue to support market expansion across Europe.

Competitive Landscape

The global semi-autonomous and autonomous bus market features a mix ofautomotive OEMs, technology providers, and mobility innovators. Key players focus on AI integration, sensor fusion, high-performance computing, and strategic partnerships.

Major companies operating in the market include:

- AB Volvo

- Bosch

- Continental AG

- Denso

- Aptiv

- NVIDIA

- Daimler

- Proterra

- EasyMile

- Navya

- Qualcomm

- Intel

- Scania

Competitive differentiation increasingly depends onsoftware intelligence, autonomous algorithms, connectivity platforms, and scalability of deployment.

Conclusion

TheSemi-autonomous Autonomous Bus Marketis entering a transformational phase, driven by urbanization, sustainability goals, technological breakthroughs, and the need for safer public transport solutions. With strong government backing, rapid advancements in AI and connectivity, and growing public acceptance, autonomous buses are set to become a cornerstone of next-generation mobility ecosystems.

{kind=link}